Can Bail Affect My Credit History?

News and ResourcesCan Bail Affect My Credit History?

TL;DR

- Bail itself does not affect your credit score.

- Courts do not report arrests, charges, or bail payments to credit bureaus.

- Your credit can be impacted by how you pay for bail.

- Financing a bail bond fee creates a loan that can hurt your score if you miss payments.

- Using a credit card for bail can increase your balance and lower your score if not paid responsibly.

- Property bonds don’t affect credit unless the property is seized or a related loan goes into default.

- Unpaid bail-related debts that go to collections can damage your credit.

- Bottom line: Bail won’t appear on your credit report — but missed payments and collection accounts will.

When a person is arrested, one of the first things that comes up is bail. Is it available for the offense in question? How much is it in this case? And what bail bond company will help me secure it quickly so my loved one or I can be released from custody as soon as possible?

Now, most people tend to think of bail as existing outside of normal time and space. That is, bail seems to be a self-contained phenomenon that exists solely within the criminal justice system. But that's not necessarily the case. In fact, there are instances when bail can interact with the broader financial system. And that raises all kinds of issues about how it may affect credit scores and credit histories.

In this guide, the team at Tayler Made Bail Bonds takes a look at how bail works, how the various credit reporting agencies view bail, and what steps you can take to minimize any impact it might have on your credit score.

How Bail Works: A Brief Overview

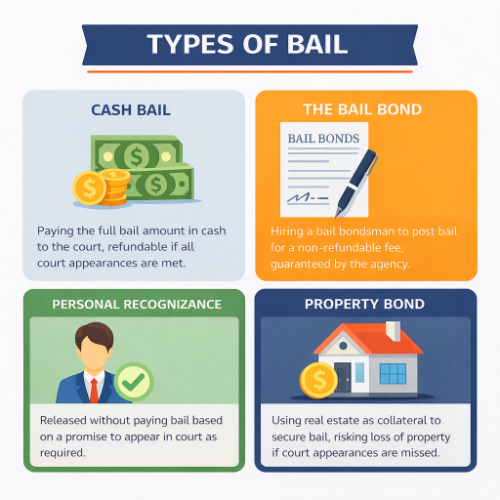

There are several forms of bail that may apply depending on the jurisdiction and the nature of the allegations against the individual. They are:

- Cash bail: With cash bail, the accused or someone acting on their behalf pays the full cash amount of bail due to the court. This money will be refunded at the conclusion of the case, provided the accused has met all their appearance obligations.

- The bail bond: Sometimes the bail amount is too high for the accused or one of their loved ones to pay in cash, in full. In that case, they seek out the help of the bail bond agent. The bonding company then provides a financial guarantee to the court in the shape of a bail bond that covers the full bail amount. In exchange, the bondsman is paid a modest, non-refundable fee for their service.

- The property bond: In some instances, a loved one may decide to offer their property as collateral for the full bail amount. The danger of the property bond is that, if the accused fails to meet all their appearance obligations, the property in question can be seized.

There is also the personal recognizance bond, under which a person is released from custody without bail solely on the promise to appear in court.

The type of bail chosen will play a central role in determining whether or not a person's credit score may be affected.

Want to learn more about the bail bonding process?

Get a step-by-step overview of how bail bonds work in Colorado and what to expect. Read the Bail Bonding Process GuideHow Credit Scores Are Determined: A Brief Overview

To understand how bail might affect a credit rating, it's helpful to understand what goes into determining a credit score. In general, a credit score is intended to reflect how responsibly a person manages borrowed money. The credit score is typically based on:

- The person's payment history: Up to 35% of a person's credit score is based on whether bills, loan payments, and credit card payments are made on time. FICO and the Consumer Financial Protection Bureau (CFPB) both note that payment history is the most important factor in most credit scoring models.

- The amount the person owes: Up to 30% of a credit score is calculated on the amount of debt a person is carrying relative to the amount of credit available to them. FICO explains that “amounts owed” — including credit utilization — are the second most influential factor after payment history.1

- How long credit accounts have been open and active: How long a person has been processing a particular debt or debts can make up as much as 15% of a person's credit score.

- New credit accounts: How often a person opens new credit accounts can affect a credit score by as much as 10%.

- The credit mix: The mix of different credit types, such as cards, loans, and more, can influence a credit score by up to 10%.

| Credit Factor | Approximate Weight |

|---|---|

| Payment history | ~35% |

| Amounts owed / utilization | ~30% |

| Length of credit history | ~15% |

| New credit | ~10% |

| Credit mix | ~10% |

Making a Direct Impact on Credit Scores

As a general rule, courts do not report cash bail payments or the use of property as collateral to credit bureaus. These transactions are self-contained within the justice system. Therefore, the only time your credit will be impacted by the bail system is if you fail to pay the person or establishment that you borrowed the money from.

That said, there are scenarios where your credit score may be dragged into the bail process. They are:

(Mis)using a bail bond agent

When enlisting the help of a bail bondsman, a person typically signs a contract agreeing to pay a non-refundable fee for the bail bondsman's services. In most cases, this fee is paid in full, upfront. But some bail bond agencies will allow you to finance this fee over time. This effectively creates a loan. If payments on this loan are missed or simply never made, and the account is sent to a collection agency, that debt may appear on a credit report, negatively affecting your credit score.

Using a credit card to pay bail

In many states, including Colorado, it is legal to use a credit card to pay bail. While this is convenient for many people, it can mean adding a significant amount to a person's revolving credit balance. Should you carry that balance over time or miss any payments, your credit score is likely to be affected.

Property bonds

If property is offered as collateral for bail, that by itself will not affect a credit score. However, if the defendant fails to appear in court and the court orders the seizure of the property to satisfy the bail obligation, the lien or mortgage default will likely be reported to credit agencies. For the person who was trying to help by putting their property up as collateral, this can be a significant secondary blow, on top of the fact that the person they were trying to help has gone fugitive.

Bail and Your Credit: Frequently Asked Questions

No. Courts and jails do not report arrests, criminal charges, or bail postings to the credit bureaus. Posting cash bail or using a property bond will not appear on your credit report by itself.

If you finance the bail bond premium and then miss payments, default on the agreement, or have the account sent to collections, that debt may be reported to the credit bureaus and could lower your score.

Offering property as collateral does not automatically impact your credit. However, if the defendant fails to appear and the court seizes the property or a related mortgage goes into default, that foreclosure or serious delinquency is very likely to be reported and can severely damage your credit.

It depends on whether the bondsman or their finance company reported the late payment or sent the account to collections. Once a late payment or collection is reported to the credit bureaus, it can remain on your credit report for years, even if you later pay the balance in full.

Borrow only what you can realistically repay, understand all financing terms before signing, set up automatic payments when possible, and prioritize staying current on any loans, credit cards, or payment plans used to secure bail.

The Bottom Line

The bottom line is that bail itself as a legal mechanism does not, by default, influence your credit score one way or another. Courts do not communicate with credit bureaus, and being arrested and posting cash bail will never appear on a credit report.

However, the way bail is financed can affect credit ratings. By using loans to pay bail, using your credit cards, or financing the fee to the bondsman, you introduce financial obligations that could end up harming your credit score by way of missed payments, collection efforts, or court judgments.

For Dependable, Affordable Bail Bonds in Jefferson County, Trust Tayler Made

If you or a loved one is in need of bail, get in touch with the team at Tayler Made Bail Bonding. There is no need for you or your loved one to spend 1 more minute behind bars than necessary. Get in touch with Tayler Made by calling us at (303) 623-0399.

Contact Info

Tayler Made Bail Bonding is available 24 hours a day and 7 days a week.

(303) 623-0399email@taylermadebailbonding.com

7220 W Jefferson Ave

Suite 200

Lakewood, CO 80235

@TaylerMadeBail